Despite the pullback, interest from Latin American and domestic buyers continues to fuel the region’s luxury sector.

Despite the pullback, interest from Latin American and domestic buyers continues to fuel the region’s luxury sector.

Colombians continued searching for Miami homes in January, according to a new report from the Miami Association of Realtors.

Potential buyers from Colombia again led a ranking of foreign nationals searching for South Florida homes using the association’s website, with 12.6 percent of the total, up from 10.5 percent the previous month. The list also includes Venezuela with 9.5 percent and Canada with 7 percent.

Foreign investment in residential real estate in South Florida totaled $7.1 billion last year, up nearly 15 percent from the previous year’s $6.2 billion. Colombian and Canadian home buyers tied for the third-most international home purchases in South Florida last year with 9 percent, each.

Check out the full list for January:

Within the U.S., those most interested in buying residential real estate in South Florida were from Texas, North Carolina, California, New York and Georgia, according to the report.

Source: The Real Deal

Wake up and smell the dirty money.

That’s the message federal regulators are sending to the real estate industry in Miami and other high-priced housing markets,

The U.S. Treasury Department announced it would extend and expand a temporary initiative designed to uncover criminals laundering money through real estate. The decree targets secretive shell companies — corporations that don’t have to reveal their true owners — buying luxury homes. The feds have already renewed the rules twice since announcing them in January 2016,

But this time, there’s a big difference — and it’s putting Miami’s struggling condo market under even more scrutiny.

The rules, previously so limited in scope that they applied only to a few hundred deals, will now cover every big-ticket cash transaction by shell companies in seven major markets. They are the South Florida counties of Miami-Dade, Broward, and Palm Beach; all five boroughs of New York City; San Antonio, Texas; Honolulu (included in the order for the first time); and Los Angeles, San Diego and San Francisco.

“This is going to gather much more information,” said Andrew Ittleman, a South Florida attorney who specializes in anti-money-laundering laws.

There’s been speculation about whether the administration of President Donald Trump, a former real estate developer, would double down on an initiative pushed by Obama-era officials. But the new policy shows Trump’s Treasury digging even deeper into the murky world of luxury real estate.

The end result: It’s going to get a lot harder for everyone from drug dealers to Latin American politicians to foreign royalty to shield purchases of U.S. condos and mansions from law enforcement.

The federal decree comes at a bad time for Miami real estate. Overbuilding and a slump in foreign buyers are hurting sales. The average sales price for luxury condo units in Miami Beach fell 21 percent year-over-year in the second quarter of 2017, according to a report from brokerage Douglas Elliman. Two-thirds of those sales were cash.

The rules kick in at different price points depending on the market. In South Florida, they apply to shell companies buying homes for $1 million or more with cash.

“This will help a market that has long neglected the amount of criminal activity taking place in the condo sector,” said Jack McCabe, a South Florida real estate analyst.

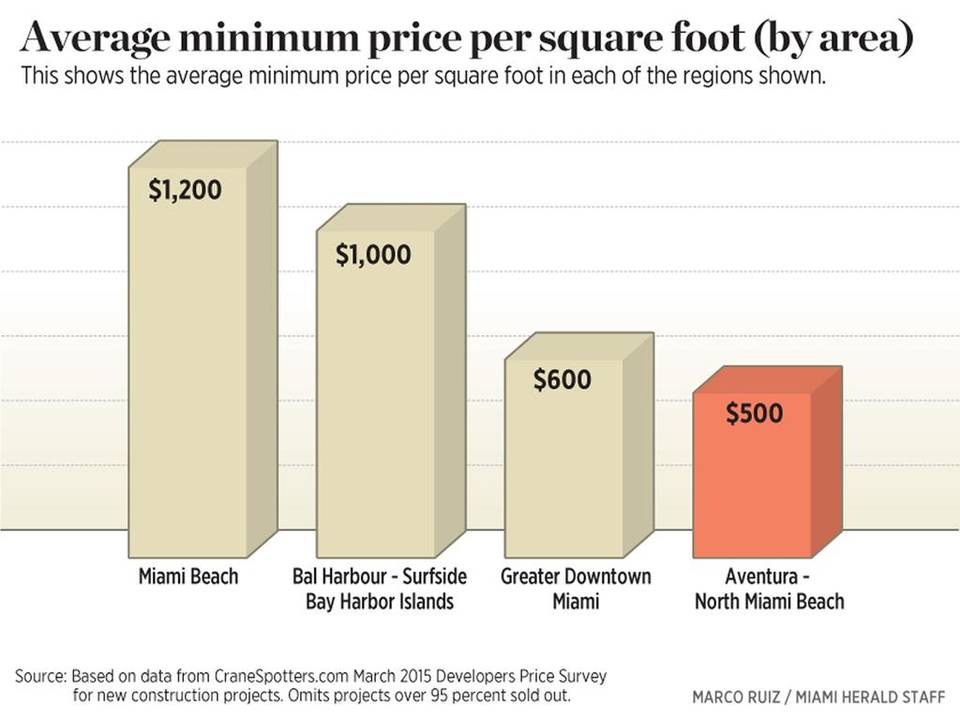

But Peter Zalewski, founder of the real estate advisory company Cranespotters, thinks the government is moving too slowly — and not going far enough.

“If you’re closing a $10 million sale and you stand to make $1 million on the deal, that’s a pretty big carrot,” Zalewski said. “And there’s no fear of a government stick, because there isn’t one in place.”

Critics dismissed Treasury’s original anti-money laundering rules — first deployed in Miami-Dade and Manhattan last year — as so narrow that they were practically toothless.

That’s because only less common methods of cash payments such as money orders, personal checks and hard currency had to be reported. But the latest order includes wire transfers, which are electronic exchanges of money between banks. In most home sales that don’t involve bank loans, money is sent from buyers to sellers through wire transfers. Regulators were missing out on a huge swath of transactions.

“It exempted most people from disclosure,” said Alan Lips, a partner at Miami accounting firm Gerson Preston. “In today’s world, people wire money.”

Until an act of Congress earlier this summer, the Treasury agency behind the initiative, the Financial Crimes Enforcement Network (FinCEN), did not have the authority to monitor wire transfers.

John Tobon, who leads a team of Department of Homeland Security investigators in South Florida, said the move is a crucial first step in allowing law enforcement to monitor funds moving electronically. After the first order, his agents observed home buyers immediately come up with “countermeasures” to avoid the disclosure requirements, including the use of wire transfers, Tobon said.

“Wire transfers were wide open” for abuse by criminals, “and no one was looking at them,” Toban said. “Now, we’re going to be able to identify companies and individuals that we had no idea about in the past.”

FinCEN is targeting cash home deals because it says they are most susceptible to money laundering. Cash transactions generally don’t involve heavy bank vetting. When banks give out mortgages, they are required to background their customers; professionals in the real estate industry are exempt from those responsibilities, although that could be changing.

As part of FinCEN’s latest push, the agency has told real estate industry professionals they should be on the lookout for suspicious activity from their clients.

“The misuse of shell companies to launder money is a systemic concern for law enforcement and regulatory agencies,” the agency wrote in an advisory to real estate agents, brokers, lawyers and other industry players.

It also encouraged them to report suspicious activity involving clients. Warning signs of bad behavior include clients willing to blindly overpay or lose money on a deal; the purchase of properties with “no regard” for their condition or location; funding that far exceeds a client’s known wealth; and clients asking for unwarranted secrecy or for records to be altered.

David Weinstein, a former federal prosecutor in South Florida who now practices white collar criminal defense, called the advisory “heavy-handed.”

“FinCEN is asking people who are not financial institutions and have no outright obligations to become an arm of the government, to become informants for them,” Weinsten said, “They’re sending a not-so-subtle message: We want you to tell us what’s going on. The implication is that if you don’t do this, we’re going to come after you and start squeezing you and say in our eyes you should have known what was going on. You should have vetted this money.”

Although real estate professionals aren’t required to set up compliance programs, no one is allowed to “willfully” turn a blind eye to money laundering, according to federal law. Weinstein recommended that realty firms consider implementing basic compliance programs.

Ron Shuffield, CEO of EWM Realty International, says the new requirement means closing agents must confirm the name and address of beneficial owners with a 25 percent stake in a corporation or limited liability company via a legal form of ID, such as a passport or driver’s license.

“There’s no legitimate buyer who’s going to feel uncomfortable with this,” Shuffield said.

The degree to which suspect money fuels Miami’s luxe real estate market is debated. But real estate crops up in case after case involving illicit funds. The release of the massive trove of offshore files known as the Panama Papers showed how easily offshore money moves into Miami real estate. The flood of cash has helped raise home prices far beyond what most locals can afford.

In FinCEN’s advisory, the agency highlighted several cases showing the threat posed by money laundering. One example cited was Venezuela’s vice president, Tareck El Aissami, and his associate, Samark López Bello. Both were sanctioned by U.S. authorities for their alleged involvement in narco-trafficking. López Bello owns three Brickell condos valued at nearly $7 million.

Tobon, of Homeland Security, said roughly 50 percent of his investigations involve money laundering through real estate.

The new order takes effect on Sept. 22 and expires on March 20, 2018. It could eventually be made permanent and expanded nationwide. The Washington, D.C., bureau of the Herald’s parent company, McClatchy, broke the news that the order would be extended Tuesday.

The FinCEN initiative — called a geographic targeting order — was designed to target the Achilles’ heel of American anti-money-laundering laws: weak transparency rules for limited liability corporations.

In many states, including Florida, it’s possible to set up an anonymous company and use it to buy a pricey mansion or condo. Offshore companies can be used for the same purpose. That’s catnip to criminals who don’t want anyone asking where they got the cash.

FinCEN changed the game by requiring title insurers — which are involved in almost all real estate transactions — to pierce the veil of shell companies and determine who really owns them. The information is not made public.

Because of the limitations of the original rules, roughly 240 transactions in the target markets were reported to regulators over 12 months, according to FinCEN data. But 30 percent of those sales were linked to people who’d been separately reported for suspicious activity by financial institutions.

In Miami-Dade, 16 of 32 reported deals were linked to suspicious buyers.

“They’re going to capture a lot more activity now,” said Jason Chorlins, a risk advisor at Miami accounting firm Kaufman Rossin. “The majority of this activity is done via wire transfer.”

Source: Bradenton Herald

An Asia Task Force organized by the Greater Miami Chamber of Commerce wants to organize Miami trips for Chinese journalists, investors and developers to help market the city to businesses and entrepreneurs from the Far East, The Real Deal has learned.

Greater Miami Chamber of Commerce’s Asia Task Force

At its first brainstorming session Friday morning, the eight-member task force laid out its objectives. Task force chairman Seth Gordon, a Miami publicist who represents Shanjie Li, the Chinese businessman whose company purchased a 2.39-acre site on Brickell Avenue for $74.7 million last year, said he wanted the Chamber to sponsor a delegation of reporters from China, who would then write articles about Miami’s business offerings. Gordon told other members he recently hosted a small contingent of eight Chinese journalists with assistance from Turnberry Associates founder Don Soffer and Carnival Cruise Lines.

“Don is very interested in working with the Chinese,” Gordon said. “He contributed a full week of rooms at the Fontainebleau Miami Beach hotel and we flew them in with eight round trip business class tickets provided by Carnival.”

While the reporters were in Miami, Shareef Malnik, owner of the Forge, had them over for dinner at the storied restaurant’s wine room, Gordon said. In addition, developers Armando Codina and David Martin briefed the reporters on their respective projects.

“If we do it as a chamber project, we can do something more serious,” Gordon said.

Peng Lu, Florida International University’s associate provost of international programs, said the college would like to coordinate events and activities, including meetings with top business leaders in Miami, for a delegation of 22 Chinese business people visiting the city in mid-September.

“Two of them are billionaires,” Lu said. “One is a frozen food king in China who wants to buy fish products from Latin America. They are all extremely interested in seeing what business opportunities are here.”

In exchange, Lu said FIU can assist the chamber in organizing a business delegation trip to important cities in China. Andy Perez, CEO of South Miami-based EB5 Visa Funds, also suggested the chamber consider sponsoring classes on how to conduct business with the Chinese.

“One of the most important things you can do is educate the chamber’s membership,” Perez said. “It’s very important, down to how you hand over your business card.”

The task force is scheduled to meet again at the end of September.

Souce: The Real Deal

High net worth investors, families, and wealth managers from Latin America, seeking to diversify their portfolios, have been on a buying binge for office buildings and single-tenant retail properties throughout Miami-Dade County during the past 18 months, real estate advisors and developers specializing in the commercial sector told The Real Deal.

“Their appetite for well-positioned income-producing assets coupled with Miami’s prospering economy are translating into appreciating property values at a faster pace than previously anticipated,” said Alex Zylberglait, president of The Zylberglait Group at Marcus & Millichap Real Estate Investment Services in Miami. “It is fueling transaction velocity across most product types. And there is particular interest in single tenant spaces.”

Alex Zylberglait, president of The Zylberglait Group

Zylberglait told TRD that his firm brokered the sale of six commercial properties to buyers from Argentina, Brazil, El Salvador and Italy in the past 15 months.

For instance, Zlyberglait represented the seller of a 20,000-square-foot office building at 1250 Northwest 57th Avenue that is the headquarters of Summit Aerospace, an aircraft maintenance company that generates approximately $18 million in sales annually. The building was sold in March of last year for $2.6 million to a company called Algafin, which lists Giorgio Rubini, an Italian national, as its manager.

4995 Northwest 72nd Avenue

In another Zylberglait brokered transaction in July of last year, a Brazilian-owned entity called Kireland 41 Street Doral purchased an L.A. Fitness at 10055 Northwest 41st Street for $9.9 million. More recently, Zylberglait represented the previous owner of an office building anchored by a Wells Fargo Bank at 4995 Northwest 72nd Avenue. The property was bought for $5.3 million on March 25 by St. Helena LLC, a corporation listing Frech Hasbun and Freddie Moises of La Libertad, El Salvador, as managers.

Zylberglait’s firm is not the only commercial real estate brokerage seeing more interest from foreign buyers. Earlier this month, Fabio Faerman of Fortune International/FA Commercial told TRD he represented a foreign buyer that purchased a 2,259-square-foot Taco Bell at 1650 Northeast 163rd Street in North Miami Beach.

“International investors are looking for business opportunities like this,” Faerman said in a statement. “This is a prime location with a great franchise, Taco Bell.”

Camilo Lopez, president and managing director of The Solution Group

The company is tearing down the old structure to make way for a Mediterranean-style office building called OFIZZINA. It will have 54 units totaling 96,767 square feet of office space, as well as three retail units at ground level and 332 parking spaces, Lopez told TRD. Camilo Lopez, president and managing director of real estate development and management company The Solution Group, said demand from Latin American buyers for commercial office space is the reason his firm is building an office condo in Coral Gables. In August of last year, Solution paid $6.6 million for a one-story office building at 1200 Ponce de Leon Boulevard, built in 1972.

“In our research meetings, we realized the office market is the least served sector in Miami,” Lopez said. “It doesn’t even reach 5 percent of the overall real estate market. Because of the very limited offerings, we decided to build a luxurious office condo building.”

The project, including the land purchase and construction, is being financed privately through a capital fund made up of investors from Latin America and Europe, Lopez said. He said the office condo concept appeals to South Americans.

Claudio Stivelman, a principal partner in Aventura-based S2 Development

Claudio Stivelman, a principal partner in Aventura-based S2 Development, said foreign investors staking claims to commercial properties in South Florida have buying power that begins in the $3 million to $5 million range.

“These are people who have likely already bought a condo or two in Miami and are looking to upgrade their portfolio,” Stivelman told TRD. “They may want to buy a Walgreens, a strip mall or a warehouse.”

In recent months, Stivelman said, his contacts in Brazil have been introducing him to investors who are not interested in condos.

“They are seeing the strength of the commercial side,” Stivelman said. “They see an opportunity to make big money.”

Zylberglait said the foreign buyers he’s dealt with view commercial properties as a safer bet.

“The income generated from the properties is a much more stable situation than buying a half-a-million dollar condo that doesn’t produce income unless you can rent it,” Zylberglat explained. “Buying a commercial asset not only produces a stronger yield. It also allows the buyers to leverage those investments.”

Source: The Real Deal

It’s a scene that’s played out countless times here in recent years.

A working-class couple identify a home they want to buy, they work with their bank on a mortgage and prepare an offer, only to find that the property’s been purchased by a foreigner who plunked down a full cash payment. “That’s happened to every Realtor in Miami,” said Adrian Foley, a lawyer and real estate agent.

That situation is partly why Miami has become one of the most expensive cities in the U.S. to buy or rent a home. Lured by the beaches or the relative security of the American real estate market, people from around the globe have flooded the area in recent years.

“Ninety percent of new construction underway in Miami right now is unaffordable for 90% of the population that lives here,” said Jack McCabe, a real estate analyst with McCabe Research & Consulting. “When people talk about this great divide between the rich and the poor,” McCabe said, “it’s very evident in Miami.”

Source: USA Today

A new strategic vision, competitive pricing and a less hectic lifestyle are three reasons North Miami Beach is emerging as an attractive location for new residential and commercial investment.

Both the scenic Biscayne Boulevard corridor and the 163rd Street commercial district are in the early stages of an exciting transformation that will bring many positive benefits and developments to the city.

Led by Mayor George Vallejo, the city of North Miami Beach adopted a strategic plan in September that sets guidelines for real-estate development, design and zoning for the next 15 years. The “visioning” framework, which was guided by two consulting firms, encourages new mixed-use projects and high-end residential towers in appropriate locations. It also includes funds for a comprehensive parks master plan, which will make the city an even more appealing place to live.

Led by Mayor George Vallejo, the city of North Miami Beach adopted a strategic plan in September that sets guidelines for real-estate development, design and zoning for the next 15 years. The “visioning” framework, which was guided by two consulting firms, encourages new mixed-use projects and high-end residential towers in appropriate locations. It also includes funds for a comprehensive parks master plan, which will make the city an even more appealing place to live.

Already, a new wave of commercial development is under way, including plans for new high-end restaurants and a hotel along West Dixie Highway south of the roadway congestion in Aventura. Gil Dezer, president of Dezer Developers in Sunny Isles Beach, purchased the Intracoastal Mall for $63.5 million last year and plans to open a luxury iPic theater in the mall this summer.

On the residential side, North Miami Beach is becoming a destination of choice for both domestic and international buyers seeking an alternative to higher-priced properties in more congested areas along the beach, in Aventura or in downtown Miami. Because the redevelopment of North Miami Beach is just in the early stages, pricing for luxury residences is more attractive than other markets that have already experienced a run-up in values.

Marina Palms Yacht Club & Residences

For example, the sales prices for the second tower of Marina Palms Yacht Club & Residences, now under development on Biscayne Boulevard, averages $550 per square foot. To the north, a residence in a new Aventura building would be $850 per square foot, and the price for oceanfront units could be double or triple that rate.

Looking back at the last few decades, it’s clear that South Florida communities are at varying stages of the real-estate cycle. For instance, South Beach real estate was a bargain in the 1980s, before a wave of new hospitality, retail and residential investment created one of the world’s most popular (and expensive) urban resort markets.

Downtown languished until the early 2000s, when new residential and mixed-use developments exploded on the scene. After the recession, developers were quick to pick up unfinished projects and market them on an all-cash basis to affluent buyers from Latin America and Europe.

Meanwhile, North Miami Beach has remained a quiet, suburban city with about 40,000 residents and great recreational amenities, such as Greynolds Park and Oleta River State Park. In addition, the Biscayne Bay campus of Florida International University is conveniently located in nearby North Miami.

With its new strategic plan in place and a growing flow of commercial and residential real-estate investment, North Miami Beach is entering a new era, just as other Miami-Dade communities have evolved in the past.

Now the world is about to discover the new “hidden gem” in South Florida’s real-estate market. It’s an exciting time to participate in the transformation process, which will create a bright future for North Miami Beach and its residents.

Source: Miami Herald

Rodolfo Ishak, developer of Krystal Tower

PHOTO: Mark Freerks

Rodolfo Ishak has had plenty of opportunities to launch his first condo project in Miami during boom cycles of years past, but he feels now is the perfect time.

Having completed more than 40 projects in his native Brazil, Ishak is making his Miami debut with Krystal Tower, a 35-story, 153-unit project at 530 N.W. First Court. It launched sales in November, starting at $342 a square foot, with an average price of $450 a square foot. It will also include 5,500 square feet of commercial space.

The property currently has a five-story shell of a project that stalled during the recession. Ishak’s company will build atop that structure. He plans to launch construction once presales reach 50 percent, he said.

A rendering of Krystal Tower, planned for 530 N.W. First Court in Miami.

Ishak and sales director Roderyck Reiter said his company and his experience has reached a level where he feels comfortable to come to Miami, a market that’s more conductive than in Brazil. His reservations are evenly divided between Brazilians and Venezuelans. Both countries are suffering from economic problems and the weakening of their currencies against the U.S. dollar.

“It has helped us in Miami because of the instability and insecurity of the economy in both countries,” Ishak said. “People who have the capital want to take their capital to a safe market like this. … It’s like a savings account to them. If they keep it in their country, they will lose value on inflation.”

Ishak said his goal with Krystal Tower is to offer the amenities residents would expect at a luxury building at a lower price point. It helps that he paid only $3.5 million for the property, compared to the tens of millions of dollars that other developers paid to obtain land near downtown Miami.

Source: SFBJ

Since its launch in Miami in 2002, Art Basel has been attracting people from all over the world who appreciate innovation and creativity.

Today, satellite events have spread to Wynwood, Midtown, downtown, Mid-Beach and North Beach, and last year about 75,000 people attended the main fair. The first Basel fair featured 160 galleries from 23 countries, attracted 30,000 visitors and has grown and grown and grown — much like our skyline and real-estate industry. The growth and popularity of the event have bolstered the tourism industry and made us one of the fastest emerging cultural epicenters of the world.

For one week in December, all eyes started looking to Miami, including those of some of the world’s greatest architects and developers. Today, they are creating a skyline that is second to none, while Basel brings buyers appreciative of artistic creations. The burgeoning love affair between Miami and art can be evidenced by two recently announced museums: the Institute of Contemporary Art, Miami, the brainchild of Norman and Irma Braman, and the Latin American Art Museum by Gary Nader. Miami was largely a blank canvas in 2002, and so many have seized the opportunity to fill the space with remarkable buildings that are works of art themselves.

In downtown Miami, Zaha Hadid paired with developers Louis Birdman and Gregg Covin for the grandiose 1000 Museum. What was once the famous Bal Harbour Club will become the spectacular, all-new Oceana Bal Harbour, thanks to Italian architect and interior designer Piero Lissoni and developer Consultatio USA. And then there is Herzog & de Meuron, Richard Meier, Norman Foster and Rem Koolhaas, among the many other great names, with others soon to be announced.

Art Basel is certainly a time for businesses to shine. It provides an instant injection of funds into the economy, and the effects of the fair linger long after it leaves town. This is certainly the case for the real-estate industry, which has benefitted greatly from the influx of discerning art lovers. Amid the week of amazing art and all the accompanying events, the glitterati look up and see Miami as a wonderful place to purchase property. And they have many to choose from, for a relatively affordable budget. All are designed by local and international architectural greats who provide a perfect place to display a new piece or two.

Daniel De La Vega, President of One Sotheby’s International Realty

The past week has seen traffic gridlock, long lines and a shortage of restaurant reservations. But as an enthusiastic collector of Latin American art and a member of the Photography Committee at the Solomon R. Guggenheim Museum, Daniel De La Vega, President of One Sotheby’s International Realty, will be sad to see the sun set on the event so soon. Art Basel will continue to play an important role in the growth of South Florida’s real-estate industry and the development of greater Miami as a whole. As a native Miamian, Mr. De La Vega is grateful for how this fair has moved the city forward in so many ways. As the tents come down and the works are carefully packed away, Miamians can still admire innovative and creative pieces all year-round.

All you have to do is look up to the skyline and thank the increased business to the bottom lines.

Source: Miami Herald

The performance of the Miami real estate market remains consistent with record activity in 2013 due to strong demand despite increased existing and new construction supply.

Median and average sales prices continue to rise, according to the latest statistics from the Miami Association of Realtors.In the third quarter, the median sales price for homes in Miami-Dade County was $250,000, an increase of 8.7% compared to last year while the median sale price for condominiums rose 3.5% to $189,900. These third quarter price increases mark 11 consecutive quarters of growth for both single family homes and condominiums.

‘The Miami real estate market continues to attract the attention of both domestic and foreign buyers, fueling solid growth and creating opportunities for both buyers and sellers, said Liza Mendez, chairman of the association’s board. ‘While there is more supply available than a year ago, there is still strong demand, and the growth of supply, new listings, sales and prices is more moderate, resulting in a more balanced market,’ she added.

In Florida the state wide median sales price for single family existing homes in the third quarter was $182,000, up 4% from the same quarter a year ago, according to the latest housing data released by Florida Realtor. The median sales price for condominiums in Florida was up 6.9% compared to the same quarter last year at $139,000. Compared to last year, the average sales prices for single family homes and condominiums in Miami-Dade County increased 14.9% to $438,431 and 3.8% to $341,927, respectively.

There were 7,632 homes and condos sold in Miami-Dade County during the third quarter of 2014, a decrease of 5% compared to the third quarter of 2013, when there was record sales activity. Sales of single family homes increased 0.2% to 3,552, while condominium sales decreased 9% to 4,080 compared with the same period in 2013.

‘In Miami, market performance continues to vary greatly depending on location, property type, price range and other factors,’ said Franciso Angulo, residential president of the Miami Association of Realtors. ‘While in most cases, increased supply is offering buyers more choices and less pressure, others are still experiencing significant competition and bidding wars,’ he explained.

He pointed out that the Miami Association’s initiatives to increase inventory and focus on assisting members to get more listings has proven successful along with some additional distressed properties coming on the market. In addition, the fact that sales remain at historically strong levels while inventory is growing points to seller confidence. Sellers are listing properties for sale because they have confidence in the market, according to Angulo.

Home and condominium listings also increased in the second quarter but by narrower margins. There were 6,237 new single family home listings during the third quarter, a growth of 5.1% relative to the same period last year. New condominium listings increased by only 1% from 8,282 in the third quarter of 2013 to 8,366 this year.

At the current sales pace, current inventory represents 5.7 months of inventory for single family homes and 8.1 for condominiums. Compared to the third quarter of 2013, months supply of inventory for single family homes and condominiums increased 13.5% and 33.6% respectively. A balanced market between buyers and sellers offers between six and nine months supply of inventory.

The median days on the market of single family home listings during the third quarter was 45 days compared to 37 days during the same period last year, an increase of 21.6%. Similarly, the median days on the market for condominium listings were 57 days compared to 46 last year, an increase of 23.9%. In the third quarter some 55% of closed sales were all cash compared to 59.2% a year ago. All cash sales were 40.4% of single family home closings and 67.5% of all condominium sales.

Since nearly 90% of foreign buyers pay cash, the association says this reflects Miami’s position as a top market for foreign buyers. Miami has a significant percentage of international buyers, generating more than double the cash transactions than the national average.

Source: NuWire Investor